Why Budgeting Is Different for Freelancers

For freelancers, a standard monthly budget doesn’t always work. After all, you never know exactly how much income will come in. Still, you can stay in control by working with averages, buffers, and a smart allocation of your income.

Step 1: Determine Your Minimum Monthly Costs

Map out your fixed expenses: rent or mortgage, insurance, groceries, and business costs such as software and equipment. This is your “survival budget”, the amount you need each month to get by.

- 📊 Create an overview of all fixed costs.

- 💡 Don’t forget to set aside money for taxes and retirement.

- 🛡️ Establish an emergency fund, for example, the equivalent of three months of fixed expenses.

Step 2: Calculate Your Average Income

Don’t focus on just one month, look at your income over the past 12 months. Divide it by 12 and use the average as your baseline. This prevents you from overspending in good months and falling short in bad ones.

Step 3: Work with a “Drawer System”

Create multiple pots or accounts and divide your income as soon as it comes in:

- 💰 Taxes (set aside 30–40%).

- 🏠 Fixed costs (your monthly survival budget).

- 🐖 Buffer (savings) to cover lean months.

- 🎯 Fun or growth (training, travel, extras).

This system prevents you from spending everything at once.

Step 4: Choose a Budgeting Method That Suits Freelancers

- Zero-based budgeting: every euro has a purpose. This works well if you’re disciplined and want full control.

- Percentage method: always divide your income into fixed percentages (e.g., 50% for fixed costs, 30% for savings, 20% for discretionary spending).

- Seasonal budgeting: ideal for freelancers with peak periods. Create a yearly budget and spread it evenly across the months.

Common Mistakes

❌ Setting aside tax money too late: leading to stress when the tax bill arrives.

❌ Not building a buffer: every dip feels like a crisis.

❌ Living as if every month were a peak month: lifestyle inflation you can’t sustain.

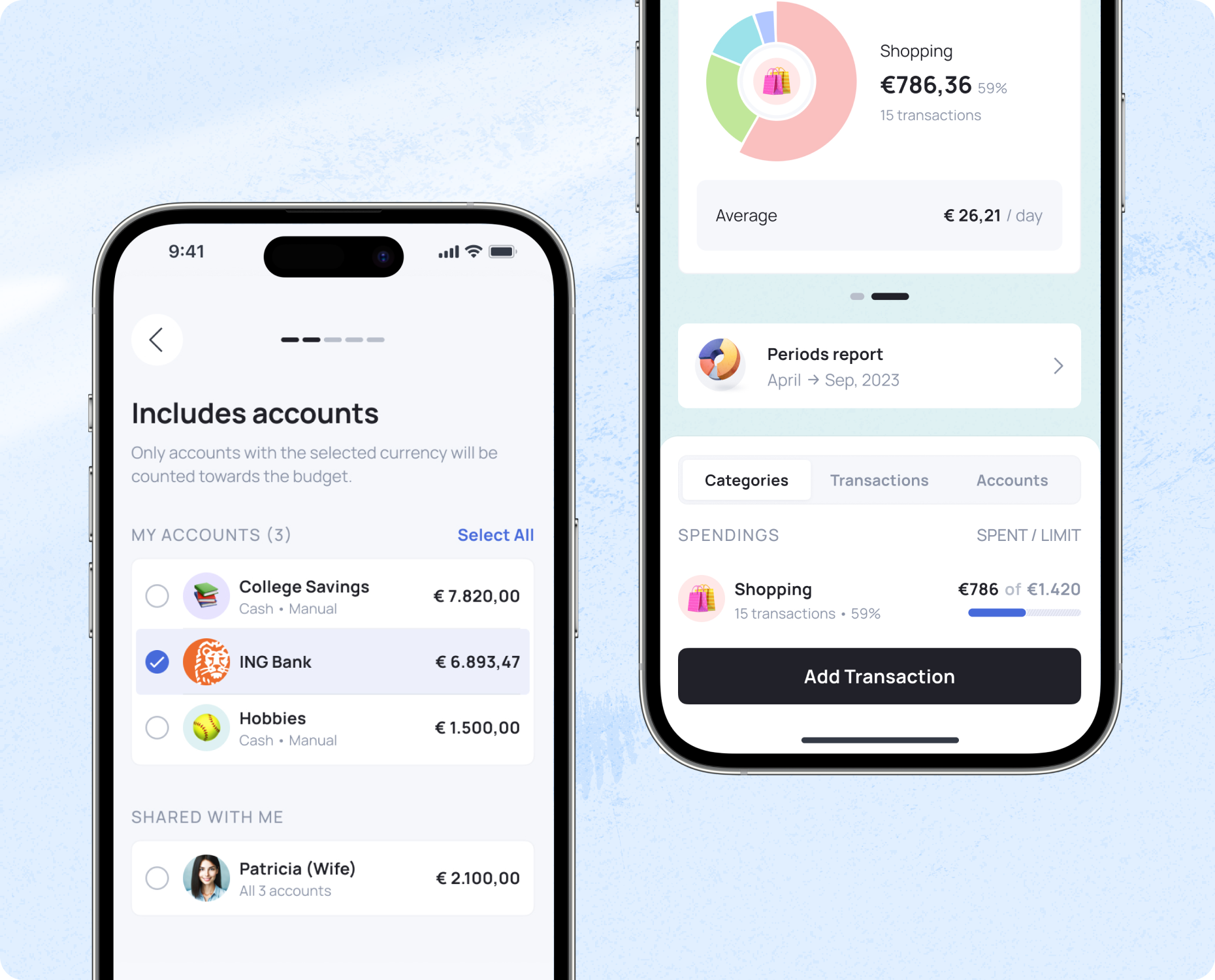

Grassfeld as a Tool

With Grassfeld, you can link your accounts so that all your transactions are categorized (don’t worry: this is largely automated). This way, you maintain a clear overview of your variable income and see exactly where your money goes. You can also set budgets per category, helping you avoid overspending during quieter months.

👉 Budgeting with a variable income requires discipline and planning, but it also brings peace of mind. By knowing your minimum costs, saving during good months, and dividing your income wisely, you ensure that you can run your business worry-free.

.jpg)