How Does a Budget Planner Work?

A budget planner helps you organise your income and expenses in a clear overview. This way, you can see at a glance how much money comes in each month, what your fixed costs are, and how much you spend on things like groceries, subscriptions, or leisure activities.

The goal of a budget planner is simple: to give you more control over your finances and prevent you from consistently spending more than you earn. Having that overview helps you spot more quickly where you can make adjustments. For example, you may decide to spend less on certain things or set aside extra money for savings goals or unexpected expenses.

Expensive and Cheaper Months

Not every month looks the same financially. Some months are more expensive, for example because of municipal taxes, holidays, festive periods, or unexpected costs. Other months may feel a bit easier financially, for example when you receive holiday pay or a thirteenth-month bonus. By mapping out these differences in advance with a budget planner, you gain more control over your finances. That way, an expensive month is less likely to catch you off guard.

What Income Do You Have?

To budget properly, it is important to first know how much money you receive each month. Are you employed? Then think of:

- Net monthly salary

- Holiday allowance, usually paid in May

- A possible thirteenth-month salary or year-end bonus, often paid in December

If you are self-employed or run your own business, you can look at your average monthly income. If you want more certainty, you can base your budget on a minimum amount.

Do you have a partner and share costs? Then include that income as well. Also, do not forget other sources of income, such as child benefits, allowances, and mortgage interest relief, which can play a role in the Netherlands.

Where Does Your Money Go?

To get started with a budget planner, understanding your expenses is just as important as knowing where your money comes from. It helps to distinguish between two types of costs: fixed expenses and variable expenses. Fixed expenses are recurring costs that always return, while variable expenses can differ from month to month.

Fixed expenses

🏠 Rent or mortgage

💡 Energy costs

📶 Internet and phone

🛡️ Insurance

📺 Subscriptions

Variable expenses

👕 Clothing

🎁 Gifts

🍽️ Going out or dining out

🚗 Transport

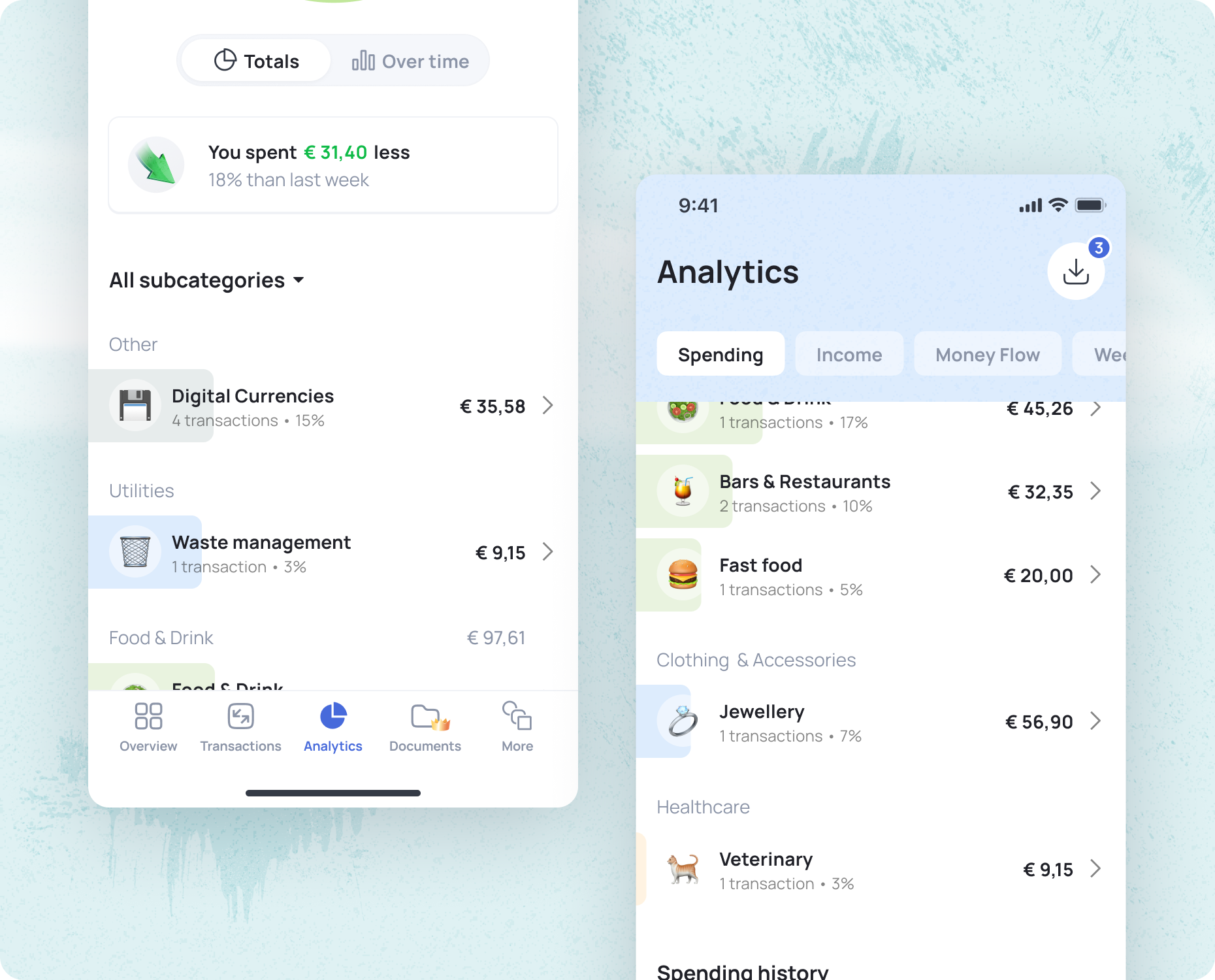

To get a good picture of these expenses, you can review your bank statements from the past few months or the past year. Another option is to use the Grassfeld app. In the app, your transactions are automatically categorised, so you can quickly see where your money is going. You can then set realistic budgets and use the app as a budget planner.

Ways of Budgeting

Many people find it helpful to set clear limits on certain types of spending. By creating budgets per category in advance, you keep more control over your money. There are many different ways to budget, so it is important to know what you want to achieve. Do you want to save more, or better align your income and expenses? Once you have a clear goal, it becomes easier to choose the method that suits you best.

Examples include:

- Envelope method: focused on limiting your spending

- Pay Yourself First: focused on saving

- 50-30-20 rule:

- 50% of your income for essential costs such as rent or mortgage, groceries, and energy

- 30% for enjoyable things such as dining out, hobbies, and entertainment

- 20% for saving or investing in the future

Also read: Learn how to budget in simple steps

Useful Tool: the Grassfeld App

The Grassfeld app can be used as a budget planner. It helps you gain insight into your income and expenses. By linking your bank account, transactions are automatically categorised and you can see exactly where your money is going.

You can then set budgets for each category. This way, you know exactly how much money you have spent in a certain area and how much room you still have within your budget. This makes it less likely that you will overspend and helps you stay in control of your finances.