1. Can You Buy a House as an Entrepreneur? 🏠

The short answer: yes. The longer answer: it depends on your figures, your business structure, and how stable your income is. In the Netherlands, you can get a mortgage as a freelancer, a partner in a general partnership (VOF), or a director-major shareholder (DGA), as long as your financial situation is sufficiently documented.

2. How Do Banks Assess Entrepreneurs for a Mortgage? 🏦

Where an employee has a permanent contract and payslips, an entrepreneur has to prove their income with figures. Banks mainly look at your business profits, the stability and continuity of your company, and any debts or loans.

To determine the maximum mortgage amount, banks usually take the average income of the past three years. If your income is declining, banks often calculate based on the lowest year. If it’s increasing, that can actually work in your favour.

3. How Long Do You Need to Be Self-Employed to Buy a House? ⏳

This differs per lender, but broadly speaking:

- 3 years self-employed: possible with almost all banks. Conditions are similar to those for employees, but the documentation is more extensive.

- 2 years self-employed: possible with some banks, under additional conditions.

- 1 year self-employed: limited options, often with higher interest rates or stricter assessments.

If you’ve been self-employed for less than three years, working with an independent, specialised mortgage advisor is almost essential when buying a house.

4. What Documents Do You Need? 📄

Applying for a mortgage as an entrepreneur or freelancer requires preparation. Banks usually ask for:

- Annual accounts from the past three years

- Income tax returns

- Income tax assessments

- An income statement (prepared by an accountant or bookkeeper)

- An overview of business and private debts

The clearer your administration, the smoother the process will be.

5. Own Funds: More Important Than for Employees 💶

For entrepreneurs, even more than for employees, the more of your own money you can contribute, the better. A lower loan-to-value ratio (borrowing less compared to the property value) significantly reduces the bank’s risk. This, in turn, increases your chances of getting a mortgage.

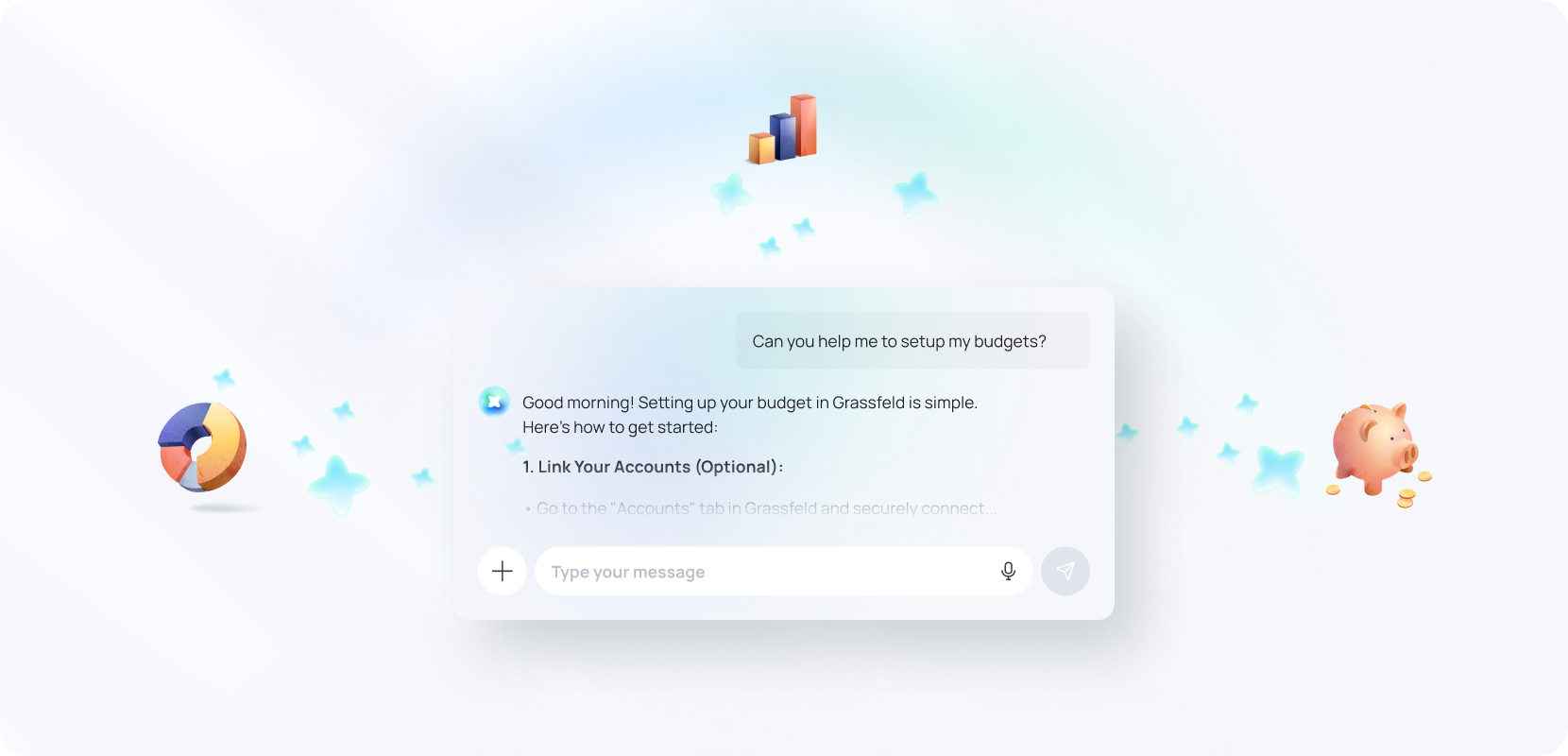

6. Get a Clear Picture of Your Finances 🔍

A mortgage application stands or falls with having a clear overview. Not just for the bank, but for yourself as well. Insight into your fixed expenses, financial buffers, and spending room makes it clear what you can realistically borrow without financial stress. With the Grassfeld app, you can easily get that overview.

By linking your accounts, your transactions are automatically categorised. This gives you insight into your fixed and variable expenses. In addition, Grassfeld shows how stable your cash flow is, since you also get an overview of all your income. This helps you make realistic choices and determine how much room you have for housing costs—even before sitting down with an advisor.

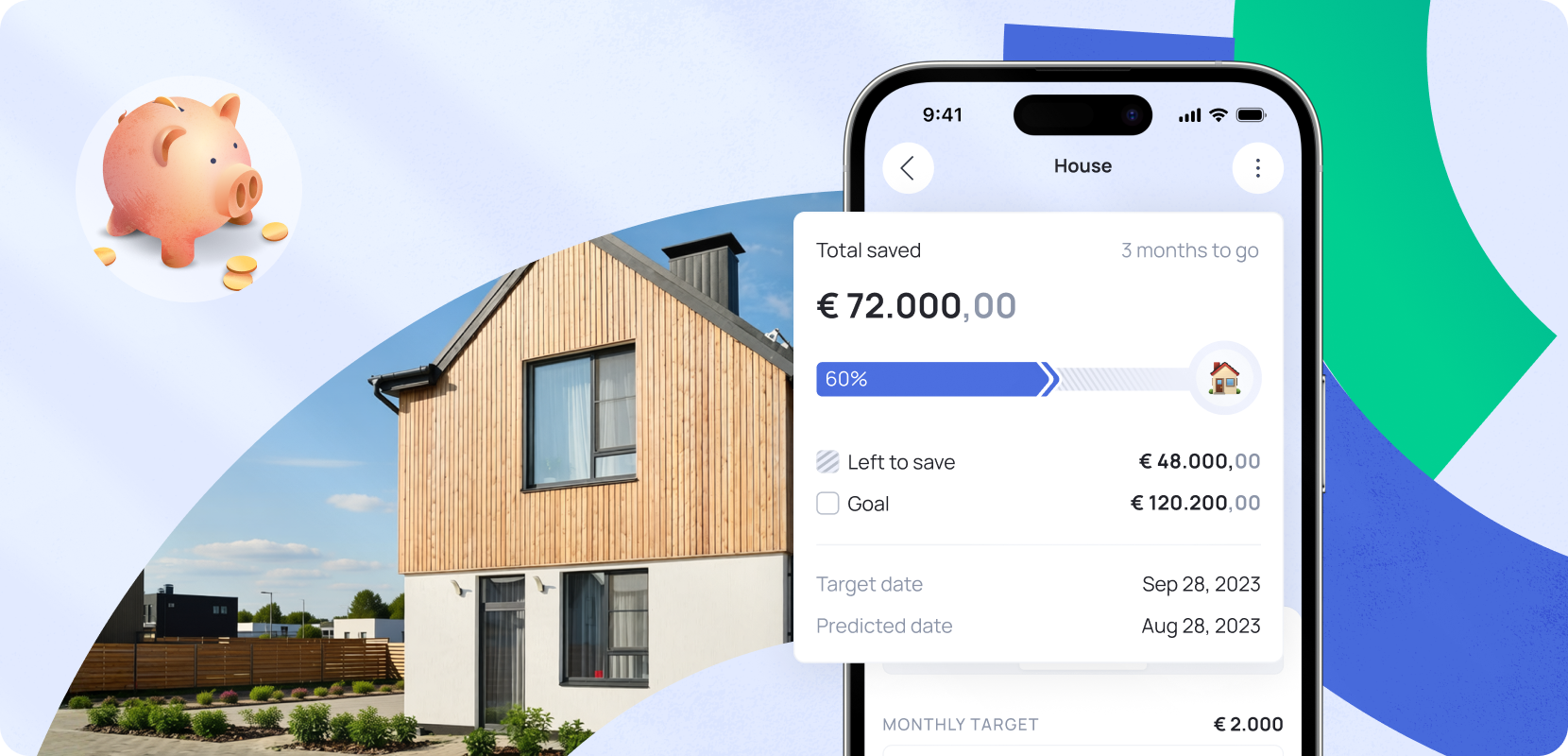

7. Savings Goals: Saving for Your Home with Grassfeld 🎯

Once you have insight, you can also figure out how much you still need to save before buying a house. With the Savings Goals feature in Grassfeld, you can make this concrete and achievable. You start by setting the total amount you need. Then you set this as a savings goal in the app. Grassfeld automatically shows how much you’ve already saved, how much you need to set aside each month to meet your deadline, and whether you’re on track.

8. Buying a House as an Entrepreneur Requires Preparation, Not Luck 🚀

Buying a house as an entrepreneur or freelancer isn’t a matter of luck—it’s a matter of preparation. With solid figures, insight into your finances, and the right guidance, there are more options than many people think.

Want to know what your financial situation really looks like before buying a house? 📲 Download the Grassfeld app now from your app store.