1. Grace Period and Repayment Phase of a Student Loan⏳

After finishing your studies, you don’t need to rush into repayment. Once student finance ends, a so-called grace period begins on 1 January of the following year. This period lasts two years. During this time, repayment is not required — although it is allowed. After the grace period, the repayment phase begins. From that point on, you’re obligated to make monthly payments towards your student loan.

2. Rules for the Monthly Payment 💵

The amount you must repay each month depends on your income and the period in which you received student finance.

If you started in 2012 or later:

- Repayment period: maximum 15 years

- Your repayment capacity is always considered

- Your partner’s income is included in the calculation

- You never pay more than 12% of your income above the repayment-free threshold

- That threshold is based on a percentage of minimum wage: 84% if single without children, 120% otherwise

- All payments are made via direct debit

If you fall under the 2018 rules (the "new system"):

- Repayment period: maximum 35 years

- You never pay more than 4% of your income above the repayment-free threshold

- The threshold is 100% of minimum wage if you’re single with no children, and 143% in all other cases

You can calculate your exact repayment amount using DUO’s official calculation tool.

3. Paying Off Your Student Loan in One Go? ⚡

Whether paying off your student loan in one go is a good idea depends on several factors. The repayment rules that apply to you play a role, but the interest rate is the most important factor.

During your studies, the interest rate is recalculated annually. Once your studies are complete, the interest becomes fixed for five years at a time. Here’s an example:

Suppose you owe €20,000 and the interest rate is set at 2.29% for the next five years (as it will be in 2026 under the 15-year system). In the first year, you’d pay roughly €450 in interest. Over five years, this amounts to approximately €2,000 (interest is calculated monthly on the outstanding balance, so the amount gradually decreases). In such a case, repaying early — whether partially or in full — can save you money. Early repayment is always penalty-free.

You can repay early in a lump sum or in instalments. The key point is feasibility. Most people can’t repay everything at once, but you can speed up repayment by increasing your monthly payments voluntarily or making one-off payments when you receive extra funds.

4. Extra Repayment Is Not Always Beneficial ⚠️

Be cautious: extra repayments don’t always make sense. Your monthly repayment is based on your income. If you earn less, you pay less — and the loan may not be fully repaid by the end of the term. In that case, the remaining debt may be forgiven. So, if you have a high student loan but a low income, early repayment might not be the most cost-effective option.

Note: payment arrears are not forgiven. You will still need to settle those.

5. On Hold ⏯️

You’re allowed to take one or more repayment pauses during the repayment phase — for up to 60 months (five years). This is helpful if you plan to travel or temporarily have a lower income. Be aware that interest continues to accrue during these pauses.

6. Getting a Mortgage with a Student Loan 🏡

A student loan can affect your mortgage eligibility. Fortunately, it’s possible to get a mortgage even if you still have student debt. However, the amount you can borrow will be lower. The higher your student loan, the smaller your maximum mortgage. In this context, repaying early can be advantageous.

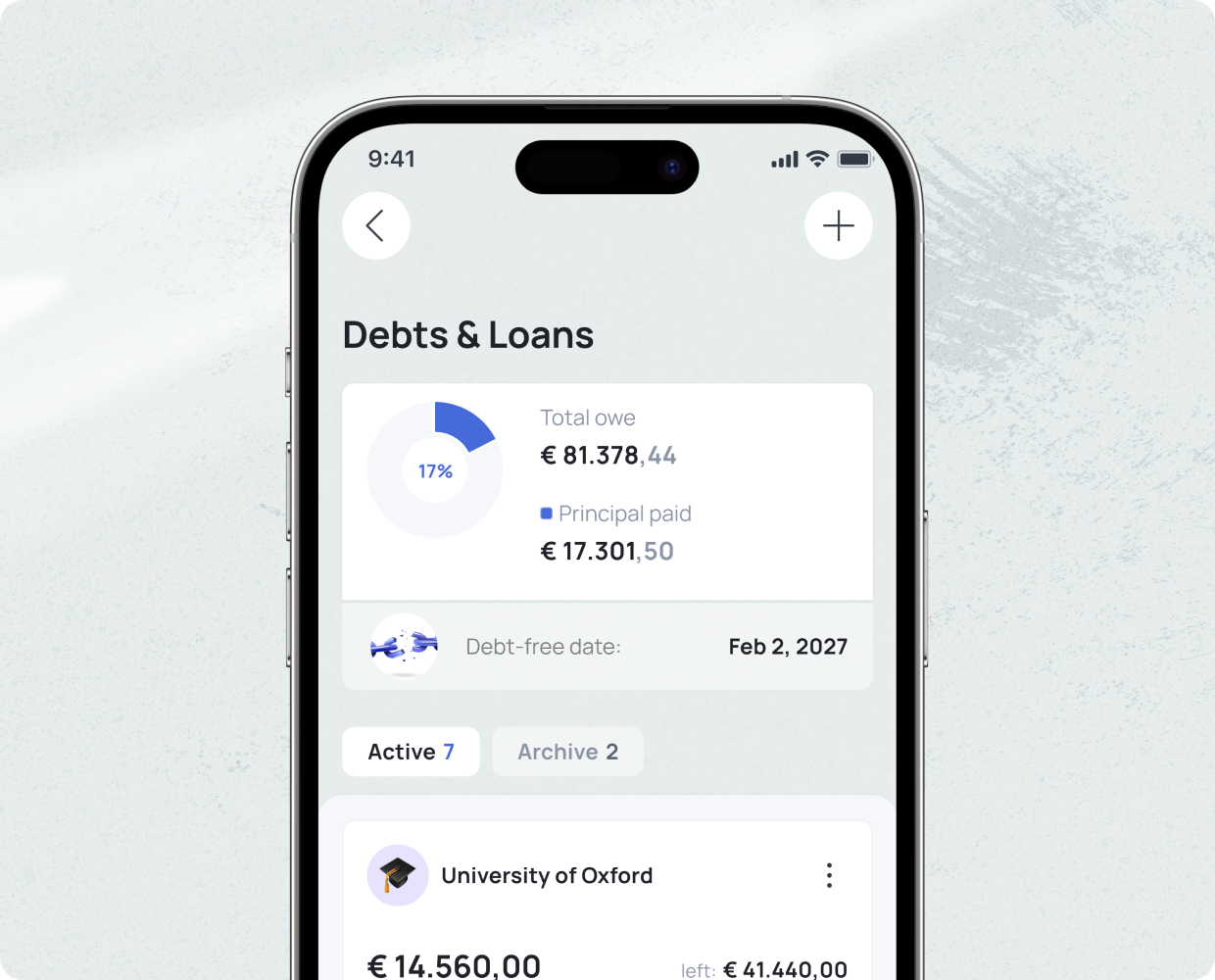

7. A Financial Overview 📊

The repayment period spans at least 15 years — and your financial situation can change significantly in that time. That’s why maintaining a clear overview of your finances is essential. How much do you earn? How much do you spend? What loans or debts do you have? Are there opportunities to improve your situation?

With the Grassfeld app, you always have a clear picture of your finances. Transactions are categorised automatically, helping you make well-informed financial decisions.

📲 Download the Grassfeld app for free from your app store today and experience the convenience for yourself.